VA Loans in Madison: A Local Hero's Guide to Buying a Home

VA Loans in Madison: A Local Hero's Guide to Buying a Home

By  John Reuter

John Reuter

|

1. What is a VA loan, how does it work, and how is it different from other loans?

A VA loan is a mortgage backed by the U.S. Department of Veterans Affairs that allows eligible veterans, active-duty service members, and some surviving spouses to purchase a home with favorable terms. What makes VA loans especially powerful in competitive markets like Madison, Waunakee, and Sun Prairie is their unique benefits:

- No down payment required (in most cases)

- No private mortgage insurance (PMI)

- Competitive interest rates

- Flexible credit and income requirements

Compared to FHA or conventional loans, VA loans are designed to reduce barriers to homeownership for those who've served our country. They're particularly helpful for buyers navigating fast-moving markets across Dane County and South Central Wisconsin.

2. Why are VA loans beneficial?

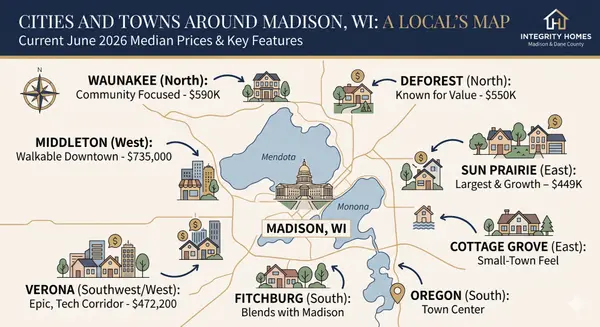

VA loans offer a significant leg-up for local heroes in our community—including veterans, law enforcement officers, nurses, and teachers—who want to buy homes in growing markets like Verona, DeForest, and Cottage Grove.

Top benefits include:

- Zero down payment for eligible buyers

- No PMI, saving you hundreds monthly

- Lower average interest rates than FHA or conventional

- Flexible approval standards, especially helpful for younger buyers or first-timers

3. Who can get a VA loan?

VA loans are available to:

- Veterans

- Active-duty service members

- Certain members of the National Guard and Reserves

- Eligible surviving spouses

You must meet minimum service requirements and obtain a Certificate of Eligibility (COE) from the VA. Many local buyers in the Madison and Sun Prairie areas are surprised to learn just how accessible this benefit is.

4. What are the major VA loan requirements?

- Occupancy: The home must be your primary residence. You must move in within 60 days of closing in most cases.

- Creditworthiness: The VA does not require a minimum credit score, but most lenders require at least a 620.

- Debt-to-Income (DTI) Ratio: The VA guideline is 41%, but lenders may approve higher with strong residual income.

- Employment History: The VA looks for stable income. Most lenders want 2 years of consistent employment, especially in healthcare, education, or public service roles.

- Residual Income: This is a VA-specific rule ensuring you have enough money left over after all bills to afford basic living costs in places like Middleton or Fitchburg.

- VA Funding Fee: This one-time fee helps keep the VA program running. It can be financed into the loan or waived for eligible disabled veterans or Purple Heart recipients.

5. What is a VA entitlement and why does it matter?

Your VA entitlement is the amount the VA guarantees on your loan. If you have full entitlement, you can borrow up to the conforming loan limit with no down payment.

In Dane County, the 2025 limit is approximately $766,550. If you've used your benefit before and haven't sold or restored your entitlement, partial entitlement rules and loan limits may apply.

6. What are the pros and cons of a VA loan?

Pros:- No down payment required

- No monthly PMI

- Competitive interest rates

- Easier to qualify compared to conventional loans

- Available in all neighborhoods, from Downtown Madison condos to suburban homes in Sun Prairie

- You must occupy the home as your primary residence

- There's a VA funding fee unless you qualify for an exemption

- Some sellers and agents still have outdated misconceptions about VA loans (this is improving, especially in our local market)

7. How do you apply for a VA loan?

a. Choose a VA-Approved Lender:

Find a lender that's experienced with VA loans—especially in South Central Wisconsin. They should understand local appraisals, market conditions, and how to advocate for VA buyers in multiple-offer situations.

b. Complete an Application:

You'll need to submit:

- Proof of income (W-2s, LES, pay stubs)

- Bank statements

- Government-issued ID

- Certificate of Eligibility (COE)

c. Get Pre-Approved:

A solid pre-approval from a VA-savvy lender gives you a major edge in hot neighborhoods like Maple Bluff, Nakoma, and the Near East Side.

d. Go House Hunting:

Work with an agent who understands VA loans and the nuances of the local market.

e. Close on Your New Home:

Once the appraisal, underwriting, and title work are done, you'll sign the final paperwork and get your keys!

8. Can you use a VA loan more than once?

Yes! Many veterans and service members in Dane County are surprised to learn that VA loans are reusable. As long as your entitlement is restored or partially available, you can use it multiple times—even while still owning another VA-financed home in some cases.

9. Can I use my VA loan for a condo or multi-family property?

Yes—if the property meets VA guidelines:

- Condos must be in a VA-approved complex

- Multi-family (up to 4 units) is allowed, as long as you live in one unit as your primary residence

There are several VA-approved condos and duplexes throughout the Madison area—ask your Realtor to check eligibility before making an offer.

10. What is the VA funding fee—and can it be waived?

The VA funding fee is a one-time charge applied to most VA loans. For first-time use with no down payment, the fee is 2.15% of the loan amount.

✅ The funding fee is waived if you:

- Receive VA disability compensation

- Are a Purple Heart recipient on active duty

- Are a surviving spouse of a veteran who died in service or from a service-connected disability

Client Reviews

"John provided top-tier service. He helped me sell my home fast and simultaneously buy a new home in Windsor, WI — a rare gem in a tight housing market. Even with limited homes for sale, John managed to find the perfect home for us and negotiated $65,000 off the list price!"

"As a nurse with a hectic schedule, I deeply appreciated his flexibility in arranging viewings that fit my irregular hours. John wasn't just our realtor; he became a trusted advisor, regularly checking in on my family and keeping us informed with market updates."

"John's expertise in the VA loan process is truly exceptional. As a mortgage lender, I've had the pleasure of working with John on multiple loan transactions, and I can't recommend him highly enough!"

Categories

- All Blogs (286)

- All Things Waunakee (11)

- Benefits (7)

- Buyer Education (5)

- Communities (19)

- Dane County Housing Market (3)

- Dane County Real Estate (4)

- Decorating (7)

- DeForest Real Estate (7)

- Deforest Wi Housing Market (16)

- Deployment (2)

- Easements (3)

- Energy Efficiency (4)

- First-Time Homebuyers (26)

- Home Buyer Tips (10)

- Home Buying (2)

- Home Inspection (2)

- Home Maintenance (3)

- Home Selling (24)

- Home Value (16)

- Homes for Heroes (8)

- Housing Assitance (7)

- Interest Rates (7)

- Madison Real Estate (4)

- Madison WI Housing Market (11)

- Market Trends (91)

- Middleton Housing Market (9)

- Middleton Real Estate (3)

- Offer to Purchase (1)

- Parade of Homes (1)

- relocation (1)

- Seller Education (4)

- Seller Tips (9)

- Sun Prairie Wi Housing Market (15)

- VA Loans (5)

- Verona Housing Market (6)

- Veterans (8)

- Waunakee Housing Market (13)

- Well, Water, Septic Systems (4)

- Windsor Real Estate (5)

Recent Posts

GET MORE INFORMATION