How the Fed Rate Cut Impacts Madison Homebuyers in 2025

How the Fed Rate Cut Impacts Madison Homebuyers in 2025

How the Fed’s latest rate cut translates into real-world decisions for Madison-area homebuyers.

Quick Answer: What the Fed Just Did & Why It Matters

On December 10, 2025, the Federal Reserve cut its key interest rate by 0.25%, bringing the target range down to roughly 3.5%–3.75%. It’s the third cut this year, and it comes as the Fed tries to support a cooling job market while keeping inflation in check.[1]

While the Fed doesn’t directly set mortgage rates, its decisions strongly influence them through expectations, bond markets, and the 10-year Treasury yield. As of early December, the average 30-year fixed mortgage rate is sitting near 6.2%—its lowest level in roughly three years.[2]

For Madison-area buyers, this cut is mostly good news: slightly better monthly payments and increased buying power. But it also risks bringing more competition and upward pressure on prices in 2026 if rates drift lower and more buyers jump back in.

🧮 What Exactly Did the Fed Change?

The Federal Reserve sets a target range for the federal funds rate—the overnight rate banks charge each other. On December 10, 2025, the Fed lowered that range by 0.25 percentage points, to about 3.5%–3.75%, in an effort to support a slowing labor market and keep the economy from stalling out.[3]

This matters for home buyers because mortgage rates are influenced by:

- Investor expectations about future Fed moves and inflation

- The yield on the 10-year U.S. Treasury, a key benchmark for fixed mortgage rates

- Overall economic outlook, risk appetite, and lender pricing

So the Fed doesn’t flip a switch on 30-year mortgage rates. Instead, its decisions help shape the direction and trend of borrowing costs over weeks and months.

📉 1. Lower Mortgage Rates (With Some Caveats)

As of early December 2025, national surveys show the average 30-year fixed mortgage rate hovering around 6.2%, down from the mid-7s we saw not long ago and now at the lowest level in about three years.[2]

Looking ahead, the Fannie Mae Economic & Strategic Research Group is projecting that 30-year mortgage rates will stay in the low-6% range through the end of 2025 and potentially dip to the high-5s by 2026.[4]

What This Means for a Typical Buyer

If you’ve been watching rates for the last two years, this is finally a little breathing room. We’re not back to 3% mortgages, but we’re also not in the 7.5% “ouch” territory anymore.

On a $400,000 loan over 30 years, moving from 6.5% to 6.0% can save roughly:

- $100–$130 per month in principal and interest

- Roughly $24,000–$47,000 in total interest over the life of the loan

That’s real money back in your budget for savings, kids’ activities, or just normal life.

Key Caveat

- Mortgage rates often move ahead of the Fed based on expectations.

- They can temporarily tick up after a cut if markets had already priced it in.

- Don’t assume every Fed cut will instantly drop the rate on your pre-approval.

💪 2. More Buying Power and More Options

Lower rates translate directly into more buying power. Here’s a simple example:

- At 6.5%, a $2,000/month principal & interest budget might qualify you for roughly a $350,000 loan.

- At 6.0%, the same monthly budget could support something closer to $370,000 (numbers will vary by lender and borrower).

That extra $20,000 in price range could be the difference between:

- A smaller starter home vs. something with an extra bedroom or home office

- Street parking vs. a two-car garage

- A house that “works for now” vs. one that fits you for the next 7–10 years

For first-time buyers, this may be the first time in a while that the payment math actually pencils out—especially if you pair a better rate with down payment assistance, VA benefits, or local grant programs.

🔥 3. More Competition & Upward Pressure on Prices

Here’s the tradeoff: cheaper money brings more buyers off the sidelines.

Nationally, the median existing-home price hit a record $435,300 in June 2025, up about 2% from a year earlier and marking more than two straight years of annual price increases.[5] Even with higher rates, low inventory has kept a floor under prices in many markets.

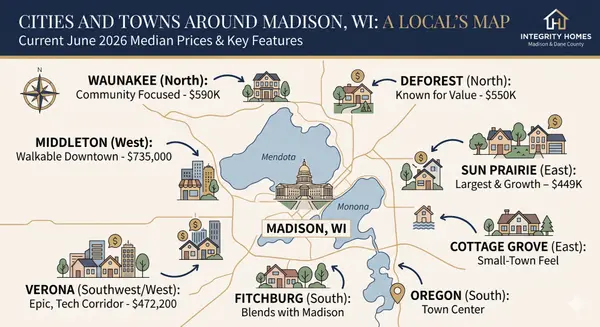

In Madison and the rest of Dane County, we’ve seen the same dynamic on a local level:

- Inventory has improved from the ultra-tight 2021–2022 days, but it’s still well below what we’d consider a true buyer’s market.

- Well-priced homes, especially between $300K and $500K, continue to move quickly.

- Many would-be buyers have been waiting specifically for rates to come down before jumping in.

What to Expect If Rates Drift Lower

- More showings and more offers on good listings.

- Potential for 2–5% price growth in hotter sub-markets over the next year.

- Less room for “lowball” offers if sellers suddenly have more options.

Fed Chair Jerome Powell has been clear: rate cuts alone won’t magically fix housing affordability because the bigger problem is still supply. There simply aren’t enough homes for the number of people who want to own one.[1]

🌐 4. Broader Economic Ripple Effects

The Fed didn’t cut rates because everything is perfect. It cut because the data is showing a cooling labor market and ongoing uncertainty:

- Unemployment is projected to drift higher than it was during the peak of the expansion, even if it stays low by historic standards.[1]

- Inflation has come down from its highs but remains above the Fed’s 2% target, which limits how aggressive they can be with future cuts.

- Economists expect home prices to grow modestly in 2026, with mortgage rates averaging just over 6% if forecasts hold.[6]

For buyers, that means two things:

- Positive: Softer conditions can open the door to more negotiation, seller concessions, or repair credits.

- Risk: If your job or income is in a shakier industry, underwriters may scrutinize your file more closely.

💳 Monthly Payment Comparison: 0.25% Can Make a Difference

Here’s a simplified look at how a small rate move changes the monthly payment on a $400,000 30-year fixed mortgage (principal & interest only):

| Interest Rate | Estimated Monthly Payment | Approx. Total Interest (30 Years) | Savings vs. Higher Rate |

|---|---|---|---|

| 6.5% (Earlier 2025 levels) | $2,528 | $510,000 | — |

| 6.25% (Post-cut ballpark) | $2,463 | $486,000 | $66/month (~$24,000 saved) |

| 6.0% (More optimistic 2026 scenario) | $2,398 | $463,000 | $130/month (~$47,000 saved) |

Note: These are rough estimates for illustration only. Actual payments depend on your credit, down payment, property taxes, insurance, and loan program. Always confirm numbers with your lender.

🎯 Practical Advice for Home Buyers Right Now

So what should you actually do with this information if you’re thinking about buying in Madison or Dane County?

1. Act Soon If You’re Already Close

- Rates are already near their recent lows. Waiting “for the bottom” is a gamble.

- If more buyers jump back in, you could face more competition and higher prices even if rates fall a bit further.

- If the monthly payment works for your budget today, strongly consider moving forward and plan to refinance later if rates improve.

2. Build in Flexibility

- Get fully pre-approved, not just pre-qualified, so you’re ready when the right home hits the market.

- Boost your down payment if possible to offset any price increases and improve your approval odds.

- Talk to your lender about rate locks, buydowns, and whether an ARM (adjustable-rate mortgage) makes sense if you know you’ll move in 5–7 years.

3. Watch the Right Indicators

- Keep an eye on the 10-year Treasury yield—it’s a big driver of fixed mortgage rates.

- Follow reputable sources for Fed expectations, such as the CME FedWatch Tool or your lender’s market updates.

- Remember: headlines lag reality. Local inventory and neighborhood demand often matter more than national noise.

John’s Bottom Line

- This rate cut is a net positive for buyers, but it’s not a magic reset to 3% mortgages.

- You’re likely to see modest payment relief and stronger competition at the same time.

- If the numbers make sense for you now, buying before the next big demand surge can be a smart long-term move.

✍️ About the Author

John Reuter is a U.S. Air Force veteran, full-time Realtor, and Broker/Team Leader of Integrity Homes of Wisconsin, brokered by Real Broker, LLC. Based in Dane County, John has spent the last decade helping buyers and sellers navigate the housing markets in Madison, Sun Prairie, Verona, Waunakee, Middleton, DeForest/Windsor, and surrounding communities with a calm, data-driven approach.

John is also the Founder and Executive Director of the Reward Our Heroes™ Foundation, a Wisconsin nonprofit dedicated to providing savings, scholarships, and support for local heroes—including veterans, active-duty military, law enforcement, firefighters, EMS, healthcare workers, and teachers.

When he’s not analyzing market stats or negotiating contracts, you’ll usually find John volunteering in the community, supporting veteran and first responder events, or talking someone through their first home purchase over coffee. Learn more about John at integrityhomeswi.com/about.

Ready to Talk Strategy for Your Next Move?

If you’re thinking about buying in 2025 or 2026, I’m happy to walk you through how this Fed decision affects your price range, payment, and timing.

📞 Call: (608) 669-4226 💬 Text: (608) 669-4226John Reuter | Integrity Homes Wisconsin | Reward Our Heroes™

Serving Madison, Sun Prairie, Verona, Waunakee, Middleton, DeForest, and all of Dane County

Categories

- All Blogs (286)

- All Things Waunakee (11)

- Benefits (7)

- Buyer Education (5)

- Communities (19)

- Dane County Housing Market (3)

- Dane County Real Estate (4)

- Decorating (7)

- DeForest Real Estate (7)

- Deforest Wi Housing Market (16)

- Deployment (2)

- Easements (3)

- Energy Efficiency (4)

- First-Time Homebuyers (26)

- Home Buyer Tips (10)

- Home Buying (2)

- Home Inspection (2)

- Home Maintenance (3)

- Home Selling (24)

- Home Value (16)

- Homes for Heroes (8)

- Housing Assitance (7)

- Interest Rates (7)

- Madison Real Estate (4)

- Madison WI Housing Market (11)

- Market Trends (91)

- Middleton Housing Market (9)

- Middleton Real Estate (3)

- Offer to Purchase (1)

- Parade of Homes (1)

- relocation (1)

- Seller Education (4)

- Seller Tips (9)

- Sun Prairie Wi Housing Market (15)

- VA Loans (5)

- Verona Housing Market (6)

- Veterans (8)

- Waunakee Housing Market (13)

- Well, Water, Septic Systems (4)

- Windsor Real Estate (5)

Recent Posts

GET MORE INFORMATION