How to Qualify for a WHEDA Loan in Madison: A Step-by-Step Guide

How to Qualify for a WHEDA Loan in Madison: A Step-by-Step Guide

WHEDA can put homeownership within reach in Madison and Dane County with down payment help and no PMI. Here is exactly how to qualify, step by step, and what to expect along the way.

How do you qualify for a WHEDA loan in Madison?

To qualify for a WHEDA loan in Madison and Dane County, you generally need a credit score of 620 or higher (640 for FHA), a household income within WHEDA's limits ($99,120 for 1–2 people, $129,800 for 3+ people in Dane County), and a completed homebuyer education course. Most buyers also need first-time buyer status (no ownership in the past 3 years), though veterans and target-area purchases are often exempt. Once those are in place, you choose a WHEDA-approved lender, get pre-approved, and apply. The full program details live on our WHEDA programs page.

If you are renting in Madison and watching prices, WHEDA, the Wisconsin Housing and Economic Development Authority, is one of the most useful tools you have. It pairs a mortgage with down payment assistance and, on conventional WHEDA loans, no private mortgage insurance. The hard part is not the paperwork. It is knowing the order of operations. This guide walks through qualifying one step at a time. For the full menu of programs and current numbers, see our dedicated WHEDA programs hub.

Quick check: are you in the ballpark?

Before the steps, here are the three gates that stop most people. If you clear these, you are very likely eligible:

- Credit: 620+ for a conventional WHEDA loan, 640+ for FHA.

- Income: household income at or below the Dane County limits ($99,120 for 1–2 person, $129,800 for 3+ person households).

- First-time status: no ownership interest in a principal residence in the past 3 years, with exemptions for veterans, target areas, and some divorced or displaced buyers.

Complete homebuyer education

WHEDA requires a homebuyer education course, and it is smart to do this first because the certificate is good for a set window and you want it ready when you apply. You can take it online or through a Madison-area HUD-approved counselor or UW Extension. The course covers budgeting, the mortgage process, and what to expect at closing, and completion rates correlate with much lower default rates down the road.

Knock this out early. It is the one step you control completely, and having the certificate in hand removes a common last-minute delay.

Confirm your income and household size

WHEDA income limits count the combined income of the adults in the household, and they vary by county and household size. For Dane County, the non-target limits are $99,120 for a 1–2 person household and $129,800 for a household of 3 or more. Target-area properties can carry higher limits.

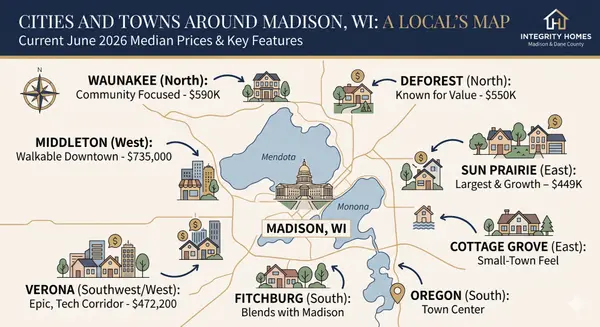

The same Dane County limits apply across Madison, Sun Prairie, Middleton, Fitchburg, Verona, Oregon, and Stoughton. If your income is near the line, this is worth confirming with a lender before you shop, because it determines which WHEDA products you can use.

Check your credit and first-time status

The minimum credit score is 620 for conventional and 640 for FHA WHEDA loans, and the underwriting is more flexible than many people expect. Rental payment history and steady employment can support an application, not just the raw score.

First-time buyer means no ownership interest in a principal residence in the past three years. Several groups are exempt:

- Military veterans (no first-time requirement)

- Buyers purchasing in designated target areas

- Displaced homemakers and single parents who previously owned a home only with a former spouse

Choose your WHEDA program

WHEDA is not one product. The pieces you are most likely to use in Madison are:

Easy Close Advantage (active)

Down payment assistance of up to 6% of the purchase price, structured as a second mortgage at the same rate as your first loan. It works for condos, townhomes, and single-family homes, and conventional WHEDA loans carry no PMI.

Tax Advantage MCC (active)

A mortgage credit certificate that can save up to $2,000 a year on federal taxes, equal to a percentage of your annual mortgage interest, for up to 30 years. This can be combined with a WHEDA first mortgage.

Capital Access DPA Currently suspended

A 0% deferred down payment loan when funded. As of the last program update it was temporarily suspended due to funding constraints, so confirm current availability before counting on it.

Gather your documents and get pre-approved

Before you apply, pull together the standard file a lender will ask for:

- Two years of tax returns

- Recent pay stubs and proof of income for all household adults

- Recent bank statements

- Your homebuyer education certificate

Choose a WHEDA-approved lender and get pre-approved. Pre-approval typically comes back in one to three business days and tells you your price range and which WHEDA products fit. Two Madison-area loan officers experienced with WHEDA are Mike Schroeder at Guaranteed Rate and Tony Burns at Fairway Mortgage.

Apply, underwrite, and close

Once you are under contract on a home, the lender submits the full WHEDA application. Underwriting usually runs 7 to 14 days, and most Dane County buyers move from contract to closing in 30 to 45 days. The biggest thing you can do to protect the timeline is keep your finances stable: no new debt, no job changes, no large unexplained deposits.

See every WHEDA program in one place

This guide is the how-to. For the full program breakdown, current limits, and a free eligibility tool, visit our WHEDA programs hub.

Frequently asked questions

What credit score do I need for a WHEDA loan?

What are the WHEDA income limits in Dane County?

Do I have to be a first-time buyer?

Do WHEDA loans require PMI?

How much down payment assistance can I get?

How long does the WHEDA process take?

Qualifying for a WHEDA loan in Madison comes down to six steps: finish homebuyer education, confirm your income fits the Dane County limits, check your credit and first-time status, pick the right WHEDA program, gather documents and get pre-approved, then apply and close. Most buyers who clear the credit, income, and first-time gates qualify.

The smartest move is to line up your education certificate and a WHEDA-approved lender early, then let a local agent help you target homes that fit the program limits.

John Reuter

Integrity Homes · Madison & Dane County

Brokered by Real Broker, LLC

All program details, income limits, and purchase price limits are set by WHEDA and the administering agencies and are subject to change. Capital Access availability noted as suspended per the most recent program update. Always verify current terms with a licensed mortgage lender before making decisions. Source: WHEDA.com. Equal Housing Opportunity.

Categories

- All Blogs (286)

- All Things Waunakee (11)

- Benefits (7)

- Buyer Education (5)

- Communities (19)

- Dane County Housing Market (3)

- Dane County Real Estate (4)

- Decorating (7)

- DeForest Real Estate (7)

- Deforest Wi Housing Market (16)

- Deployment (2)

- Easements (3)

- Energy Efficiency (4)

- First-Time Homebuyers (26)

- Home Buyer Tips (10)

- Home Buying (2)

- Home Inspection (2)

- Home Maintenance (3)

- Home Selling (24)

- Home Value (16)

- Homes for Heroes (8)

- Housing Assitance (7)

- Interest Rates (7)

- Madison Real Estate (4)

- Madison WI Housing Market (11)

- Market Trends (91)

- Middleton Housing Market (9)

- Middleton Real Estate (3)

- Offer to Purchase (1)

- Parade of Homes (1)

- relocation (1)

- Seller Education (4)

- Seller Tips (9)

- Sun Prairie Wi Housing Market (15)

- VA Loans (5)

- Verona Housing Market (6)

- Veterans (8)

- Waunakee Housing Market (13)

- Well, Water, Septic Systems (4)

- Windsor Real Estate (5)

Recent Posts

GET MORE INFORMATION